Morocco’s petroleum resources are largely unexplored, offering the opportunity for attractive exploration and development initiatives to supply a significant domestic natural gas market. Morocco has strong, long-term demand that reflects North African and European pricing.

Morocco Facts

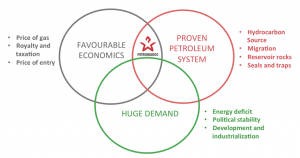

Morocco is a fiscally favourable natural gas market with strong, long-term demand and access to North African and European gas pricing.

- Capital: Rabat

- Official language: Arabic

- Area: 710,850 square kilometres

- Population: 32 million

- Chief products: Agriculture, manufacturing, mining – phosphate rock, phosphoric acid

- Political system: Constitutional monarchy under a hereditary king. The legislature has two houses – the Chamber of Representatives, members elected directly, and the Consultative Chamber, members chosen by electoral college. The king appoints the prime minister and cabinet.

Gas Monetization Opportunities

| Undersupplied | - Morocco imports 99% of oil, 91% of gas

- Africa’s second largest importer

- Energy bill of US$13 billion, half of the trade deficit

|

| Strong domestic market | - Energy demand up 54% over last decade, on steady rise

|

| Electricity | - Potential gas conversion into electricity

- Tahaddart: gas intake capacity 49 mmcf/day

- Ain Beni Mathar: gas intake capacity 34 mmcf/day

- 80% of electricity primary energy source is thermic

|

| Phosphate industry / OCP | - Gas to support local industry

- Morocco is home to 85% of the world’s known phosphate reserve

- African Development Bank loaned $250 million to OCP for industrial platform at Jorf Lasfar

- Moroccan exports as share of world trade: 32% phosphate rock, 11% fertilizers

- OCP plans to double production of rock and triple production by 2020

|

| Fundamental economics | - Competitive gas price

- Spot condensate price

|

Political & Economic Stability

| Political stability | - Only North African political regime unaffected by Arab Spring

- Constitutional Monarchy

- Democratically elected government

- Stable political system and secure operating environment

|

| Rapid economic growth | - 4.4% CAGR GDP growth (2005-2010)

- Foreign investment of US$45 billion in 2011

- Four times higher than in 2001

|

Fiscal Terms

| Fiscal incentives | - 25% state participation

- Royalty: oil 10%, gas 5%

- 10 year corporate tax holiday on discovery

|

| | |

Exploration Activity

| Underexplored | - Well density of just 0.06 wells per 100 square kilometres vs. estimated global average of 2 wells per 100 square kilometres

- 3,500 kilometres of coastline with only 31 wells drilled offshore

- Many sedimentary basins remain sparsely explored

|

| Increasing exploration | - 12 times as many exploration permits in 2012 than 1997

|